A recurrent problem in

regression analysis is the omitted variable bias: if you estimate a regression

and you do not include on the right side a variable that belongs to the model

and is correlated with some included variables, the OLS estimates will be biased.

The gist of this post is whether we have something of an analogous problem in

addressing the current macroeconomic problems in the €-area, namely by not

considering the possible influence of income distribution.

Of course, I am aware

that some economists consider unequal income distribution a critical issue, for

instance E. Stockhammer titles one of his paper: Rising Inequality as a

Root Cause of the Present Crisis [1]. However, this

approach has not really entered the main policy discussions, may be just

because it has been formulated in a somewhat extreme way, giving too central a

role to income distribution.

The emphasis in this

post is on the German situation, also because the huge German current account

is something of an embarrassment for those, like me, who think that there is a

lot to appreciate in the way the German economy is managed, but cannot just

ignore the recurrent critique [2] that the

insufficient domestic demand in Germany, and the resulting huge current account

surplus, is a problem for the €-area and, ultimately, for Germany itself. The

overall question raised in this post is whether a higher remuneration of

labour, and its close empirical counterpart of more equality in income

distribution, would not contribute to increase domestic demand in Germany and

thus reduce its mammoth current account surplus.

I used the term "contribute" in the previous sentence on purpose: there is no pretence that paying German workers more would be "the" solution to the excessive current account surplus of Germany. I think, however, that it is useful to raise the question whether such a change should be part of the solution.

An answer to this question is made more difficult by the fact that economics is a science not hard enough to be free of political preferences: left-wing economists will always say that there is too much income going to profits and top earners, right-wing economists will constantly say the opposite. It is clear, instead, that there is an optimum functional and interpersonal income distribution and that actual distribution may move away from that optimum in either direction, making fixed views not appropriate. In this post I will attempt to maintain a balanced approach and make the conclusion depend on the reasoning rather than the opposite. In order to do so, I will very briefly recall two concepts of income distribution: functional and interpersonal distribution, then I will summarily report what we know about long term trends of income distribution at international level, in particular over a medium term horizon, before moving to the specific case of Germany. I will then address the links between income distribution, on the one hand, and domestic demand and the current account, on the other hand. Short remarks on policy aspects will close the post.

Conceptually there are two different definitions of income distribution: the functional one, between labour and capital, and the interpersonal one, between rich and poor or, in drier language, between high and low percentiles in the distribution of income. Empirically, however, the two definitions are correlated, given that capital is very heavily concentrated in the hands of rich people and when capital remuneration goes up rich people become richer [3] .

The three prevailing long term empirical trends at global level regarding income distribution, at least since the end of the seventies, have been:

- An increase of capital

income [4];

- Increasing inequality among different

income percentiles within most advanced and emerging

economies [5];

- Decreasing inequality across

countries, especially because of the vertiginous growth of China over the

last few decades.

The joint effect of the increase of

within-countries inequality (e.g. rich American got richer and poor American

got relatively poorer) and the reduction of across-countries inequality (e.g.

the distance between average American and average Chinese got smaller) produced uncertain

effects on global inequality, i.e. the inequality among the entire global

population, with some economists even identifying a decrease of inequality [6]. In a secular

perspective, Bourguignon and Morrisson measure a broad stabilisation in

inequality after World War II and until the end of their period of

analysis at the beginning of the nineties, following a trend, of strong

increase since 1820. [7].

The developments in

Germany are quite consistent with the first two points mentioned above about

global developments:

- In the eighties and

nineties [8] the share of labor in income distribution came

down by some 8 percentage points, and it came down some further 5

percentage points in the first decade of the new

century, even if, due to the cyclicality of profits,

the labour share went somewhat up during the recession towards

the end of the decade [9],

- Interpersonal inequality grew in the seventies

and eighties by some 3 per cent (as measured by the Gini coefficient in

Harjes [10] and

by a further 3 per cent in the first decade of the new millennium (again

as measured by the Gini index, in Schmid and Stein, Op. Cit. pg. 19).

The macroeconomic

consequences of a move in income distribution toward capital and towards more

inequality are obvious. The most evident effect is on consumption as the

propensity to consume out of capital income is much lower than that out of wage

income and the propensity to save increases very sharply moving from

lower to higher income classes (from just above 4.0 per cent for the lowest

quartile of the distribution to close to 16.0 per cent for the highest

quartile in Germany) [11]. On the other hand, as long as the decrease in

profits influences investment more than the prospects of higher

consumption, an increase of the capital share and of inequality in the

distribution of income will have a negative effect on investment. In addition,

as a consequence of higher domestic demand and a possible effect of a higher

labour share on export prices, there will also be a downward effect on the

trade balance.

Stockhammer and Onaran [12] report a possible quantification of the

macroeconomic effects in the euro area of an increase of the capital share in

income distribution. Lavoie

and Stockhammer [13] report similar quasi-multipliers for a number of

economies, including Germany, which has similar parameters to those estimated

for the €-area. The relevant values are reported in table 1.

Table 1: Effects of a 1% increase in the profit

share

Consumption

|

Investment

|

Net exports

|

Private excess

demand

|

|

A

|

B

|

C

|

D(A+B+C)

|

|

Euro area‐12

|

‐0.439

|

0.299

|

0.057

|

‐0.084

|

Germany

|

‐0.501

|

0.376

|

0.096

|

‐0.029

|

A back of an envelope

calculation, based on the estimates of the increase of the profit share for

Germany reported above for the last three decades and the quasi-multipliers in the

table above, would indicate that consumption would have been more than 5 per cent

higher in Germany if capital remuneration had remained at the level prevailing

at the end of the seventies, investment and the trade balance would

have been some 4 per cent lower and 1 per cent lower respectively.

Of course the

quantification of the macroeconomic effects of an increase of the labour share

in income distribution would require a much more

careful empirical exercise than the back of the envelope estimates

above. One issue, in particular, which I think should be further

explored is whether the negative effect on investment would be currently as

strong as reported in the table above. Two reasons make this question

particularly relevant: first, as income distribution moved in favour

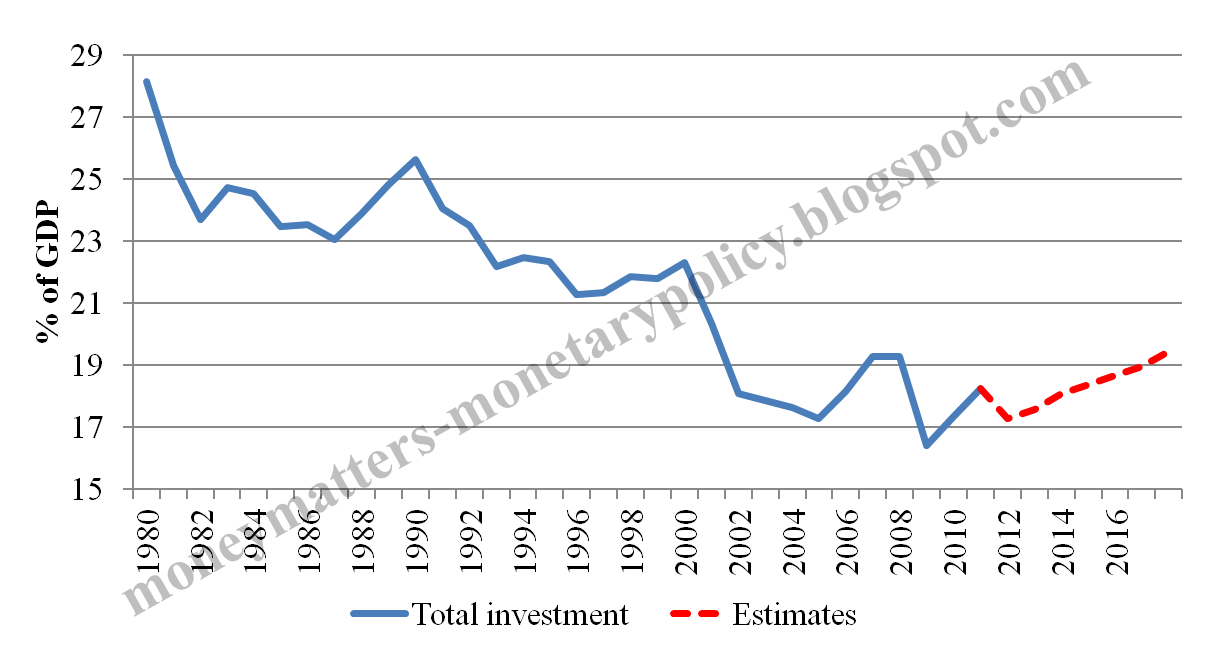

of profits over the last three decades, investment in Germany has

moved down quite a lot (see Chart 1) instead of growing, second, a strong

accelerator effect may reduce the negative effects of lower profits on

investment because of the positive prospective effect on consumption.

Chart 1: Total investment as percent of GDP: Germany 1980-2018

|

| Source: IMF WEO, October 2013 |

Even taking into account

the uncertainty about the quantitative effects, the qualitative conclusion is

clear: better remuneration for labour, and the consequent reduction in income

inequality, in Germany would help rebalance the economy from excessive reliance

on foreign demand.

The further question that immediately arises, however, is what tools a government has to influence income distribution. Pay in the private sector is and should remain a decision of firms and workers. This principle, however, should not be translated into its caricature: that income distribution between capital and labour follows mechanically the respective marginal productivities. Social factors and government action do have an influence on income distribution. The tax system is a first, obvious tool in the hand of the government. It is interesting, in this respect, that Schmid and Stein measure a reduced ability of the tax system in Germany to redistribute income towards lower income levels since 2003. The government can also have an influence on income distribution by its own wage policy: raising wages in the public sector produces an effect in the private sector as there is competition in attracting workers between the two sectors. Finally, the government can promote a social climate generally in favour of higher labour remuneration, beyond the bland statements to this effect issued by some German government representatives [14]. It is, however, unclear how much fixing a minimum wage, as recently done in Germany, helps in redistributing income.

In

conclusion, the tentative answer to the question in the title of this post is

that, yes, European macroeconomic imbalances would be attenuated if German

workers got higher wages and this could be done without damages to the German

economy: the issue is not to worsen German competitiveness and

make the economy weaker, but just to better remunerate the very high

productivity of German workers, tilting income distribution in their

favour. An additional benefit for the rebalancing of the European economy would

be that higher wages in Germany would allow a recovery of competitiveness in

the periphery of Europe with respect to Germany without forcing wages in the

negative territory, thus risking bringing the entire euro area into deflation.

*** Research assistance was provided by Mădălina Norocea

[1] Engelbert Stockhammer, Rising Inequality as a Root Cause of the Present Crisis, PERI working paper No 282, April 2012

[2] US Treasury: “Germany has maintained a large current account surplus throughout the euro area financial crisis, and in 2012, Germany’s nominal current account surplus was larger than that of China. Germany’s anaemic pace of domestic demand growth and dependence on exports have hampered rebalancing at a time when many other euro-area countries have been under severe pressure to curb demand and compress imports in order to promote adjustment. The net result has been a deflationary bias for the euro area, as well as for the world economy” Semiannual Report on International Economic and Exchange Rate Policies, Oct 2013

[11] Ulrike Stein, Zur Entwicklung der Sparquoten der privaten Haushalte – Eine Auswertung von Haushaltsdaten des SOEP, DIW, Dec 2009

[1] Engelbert Stockhammer, Rising Inequality as a Root Cause of the Present Crisis, PERI working paper No 282, April 2012

[2] US Treasury: “Germany has maintained a large current account surplus throughout the euro area financial crisis, and in 2012, Germany’s nominal current account surplus was larger than that of China. Germany’s anaemic pace of domestic demand growth and dependence on exports have hampered rebalancing at a time when many other euro-area countries have been under severe pressure to curb demand and compress imports in order to promote adjustment. The net result has been a deflationary bias for the euro area, as well as for the world economy” Semiannual Report on International Economic and Exchange Rate Policies, Oct 2013

IMF: “significantly smaller current account would be useful” David Lipton, American Academy speech, Oct 2013

EC: “We do need to examine this further and understand whether a high surplus in Germany is something affecting the functioning of the European economy as a whole” Jose Manuel Barroso, referring to the in-depth economic analysis of Germany, launched in Nov 2013

[3] Adler and Schmid, Factor Shares and Income Inequality — Empirical Evidence from Germany 2002-2008 , DIW Berlin, Apr 2012

[4] Florence Jaumotte and Irina Tytell , How Has The Globalization of Labor Affected the Labor Share in Advanced Countries, IMF Working Paper Research Department, Dec 2007

[5] Branko Milanovic, More or Less, IMF Finance & Development, Vol. 48, No.3, Sept 2011

Anthony Atkinson, Income Inequality in OECD Countries: Data and Explanations, CESifo Working Paper, No. 881, Feb 2003

Pinelopi Koujianou Goldberg and Nina Pavcnik Distributional Effects of Globalization in Developing Countries, NBER Working Paper No. 12885,Feb 2007

Giovanni Andrea Cornia, The Impact of Liberalisation and Globalisation on Income Inequality in Developing and Transitional Economies, CESifo Working Paper No.843, Jan 2003

[6] Xavier Sala-i-Martin, The Disturbing “Rise” of Global Income Inequality, NBER Working Paper 8904,Apr 2012

[6] Xavier Sala-i-Martin, The Disturbing “Rise” of Global Income Inequality, NBER Working Paper 8904,Apr 2012

[7] François Bourguignon and Christian Morrisson, Inequality among World Citizens: 1820-1992 , The American Economic Review, Vol. 92, No. 4, Sept 2002

[8] Thomas Harjes, Globalization and Income Inequality: A European Perspective, IMF Working Papers, July 2007

[8] Thomas Harjes, Globalization and Income Inequality: A European Perspective, IMF Working Papers, July 2007

[9] Kai Daniel Schmid and Ulrike Stein, Explaining Rising Income Inequality in Germany, 1991-2010, IMK, Sept 2013

[10] Thomas Harjes, Globalization and Income Inequality: A European Perspective, IMF Working Paper, European department, July 2007[11] Ulrike Stein, Zur Entwicklung der Sparquoten der privaten Haushalte – Eine Auswertung von Haushaltsdaten des SOEP, DIW, Dec 2009

[12] Ozlem Onaran and Engelbert Stockhammer, Rethinking wage policy in the face of the Euro crisis. Implications of the wage-led demand regime, International Review of Applied Economics Vol. 26, No. 2, Mar 2012 report the estimates from Onaran, Ö., and Galanis. 2011, Wage-led and profit-led demand: A global mapping. Paper presented at the workshop on ‘Wage-led growth: An alternative to finance-led capitalism?"

[13] Marc Lavoie and Engelbert Stockhammer, Wage-led growth: Concept, theories and policies, ILO, 2012 report the estimates from Onaran and Galanis, reported in footnote 10

[14] “It is fine if wages in Germany currently rise faster than in other EU countries. These wage increases also serve to reduce the imbalances within Europe.” Wolfgang Schäuble, May 2013

Very interesting. It would be also interesting to investigate the roots of the shifts in the income distribution occurred in the last two three decades. It would be important also to shape policies.

ReplyDeleteIt is striking that there seem to be a common trend across countries with different level of regulation, labour market, degree of unionisation … Must be something more structural. Technology?

Many thanks for your comment. Indeed technology and globalisation are often quoted as important global determinants of inequality in advanced economies. In emerging economies, and particularly in China, it is more a dual economy issue, with a poor agriculture and a modern industrial sector. In terms of policies, the short term ones are for redistribution through the budget, which only go so far, while the more important long term should be cared by education and promotion of social mobility.

DeleteBest regards,

Francesco Papadia